TOMS VAT on Margin: How Automatic Calculation Saves Hours

The Tour Operators Margin Scheme explained simply. How to calculate VAT on margin correctly and why automation eliminates costly errors.

What is TOMS?

The Tour Operators Margin Scheme (TOMS) is an EU VAT regime that applies to businesses selling travel packages. Instead of charging VAT on the full selling price, you only pay VAT on your margin — the difference between what you charge the client and what you pay suppliers.

TOMS exists because travel packages typically combine services purchased in multiple EU countries, each with different VAT rates. Without TOMS, an agency selling a package including a hotel in Spain, a transfer in France, and an excursion in Italy would need to register for VAT in each country and apply local rates to each component. TOMS simplifies this by allowing the agency to account for VAT only in their country of establishment, calculated solely on the margin.

The scheme applies to any business acting as principal (not agent) in the supply of travel services. This includes traditional travel agencies selling packages, tour operators, and increasingly, online platforms that bundle services. If you buy services from third-party suppliers and resell them as part of a package to the end consumer, TOMS almost certainly applies to your business.

It is important to note that TOMS is mandatory, not optional. If your business falls within its scope, you must use it — you cannot choose to apply standard VAT rules instead. The penalties for non-compliance can be severe, including back-taxes, interest, and fines from tax authorities.

Why manual TOMS calculation is risky

Calculating TOMS manually means tracking every supplier cost, computing the margin per service, applying the correct VAT rate (which varies by country), and documenting everything for tax authorities. One mistake can mean underpaying VAT (penalties) or overpaying (lost profit).

The complexity multiplies with every booking. A typical package might include 8-12 individual services from different suppliers, each with its own cost, currency, and payment timeline. Some costs are known at booking time (hotel rates), while others are estimated and finalised later (fuel surcharges, local taxes). The margin — and therefore the TOMS VAT — changes every time a cost is updated.

Manual calculation also creates audit risk. Tax authorities can request detailed documentation showing how TOMS was calculated for any booking within the statute of limitations (typically 5-7 years). If your calculations live in disconnected spreadsheets with no version history, reconstructing the audit trail becomes a nightmare. Agencies have been fined not because their calculations were wrong, but because they could not demonstrate how they arrived at the figures.

The most common manual errors include: forgetting to include ancillary costs (transfers, insurance, visa fees) in the supplier cost base, applying the wrong VAT rate after a rate change, failing to adjust the margin when supplier costs are updated post-booking, and double-counting costs that appear in multiple documents. Each of these errors either increases your tax liability or reduces your reported margin — both costly outcomes.

The formula

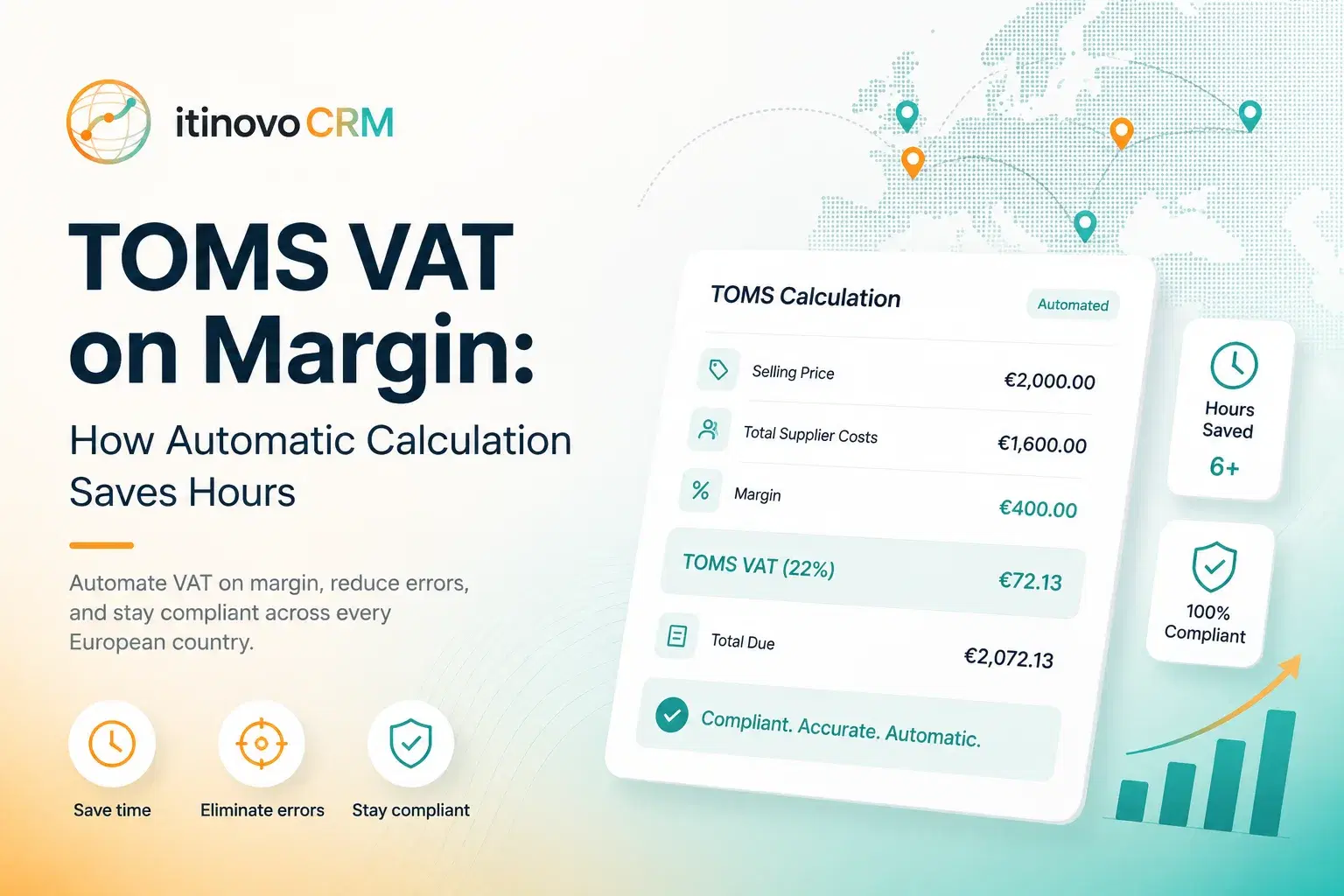

TOMS VAT = (Selling Price - Total Supplier Costs) x VAT Rate / (100 + VAT Rate). For example, if you sell a package for 2,000 EUR and supplier costs are 1,600 EUR, your margin is 400 EUR. In Italy (22% VAT): TOMS VAT = 400 x 22/122 = 72.13 EUR.

Let us break this down further with a realistic example. You are selling a 7-night package to Sardinia:

Hotel (7 nights double room HB): 980 EUR. Transfer airport-hotel return: 120 EUR. Guided excursion: 85 EUR. Travel insurance: 45 EUR. Total supplier costs: 1,230 EUR.

You sell the package to the client for 1,650 EUR. Your margin is 1,650 - 1,230 = 420 EUR. In Italy, the TOMS VAT on this margin is: 420 x 22/122 = 75.74 EUR. Your net margin after VAT is: 420 - 75.74 = 344.26 EUR.

Note that the VAT is extracted from the margin (it is VAT-inclusive), not added on top. This is a common source of confusion. The client pays 1,650 EUR total — the TOMS VAT is already embedded in that price. You do not add 22% on top of the selling price.

For agencies operating in multiple countries or selling to clients in different member states, the calculation becomes more complex. The VAT rate applied is always that of the country where the agency is established — not where the services are consumed or where the client resides. This is one of the simplifications that TOMS provides.

How automation works

A travel CRM with built-in TOMS calculates this in real-time as you build the quote. Every time you add a service with a cost, the margin and VAT update instantly. When you generate an invoice, the TOMS line is pre-calculated and compliant.

The automation works at multiple levels. At the quote level, every service you add includes both a cost (what you pay the supplier) and a selling price (what the client pays). The system continuously computes the aggregate margin and the corresponding TOMS VAT. Visual indicators show your margin percentage in real-time — green when healthy (above 15%), amber when thin (8-15%), and red when dangerously low (below 8%).

At the invoice level, the system generates the correct tax line automatically. For Italian agencies, this means a single line showing the TOMS VAT amount with the appropriate regime code. For French agencies, the Factur-X XML includes the correct VAT category (O for TOMS) with the legal reference to Art. 266-1 CGI. The agency never needs to manually calculate or enter these figures.

When supplier costs change after the quote is sent — which happens frequently with seasonal rate adjustments, currency fluctuations, or confirmed prices differing from quoted estimates — the system recalculates the margin and VAT automatically. If the margin drops below a configurable threshold, the system alerts the agent, who can then decide whether to absorb the difference or renegotiate with the client.

The audit trail is maintained automatically. Every version of the quote, every cost change, and every invoice generated is timestamped and stored. If a tax authority requests documentation for a specific booking, the system can produce a complete history showing exactly how the TOMS calculation evolved from initial quote to final invoice.

Country-specific rules

Italy uses 22% standard rate. France uses 20% with specific Chorus Pro requirements. Germany uses 19% (Margenbesteuerung nach Par. 25 UStG). Spain uses 21% (Art. 141-147 Ley 37/1992). A good CRM handles all of these automatically based on your agency's country.

In Italy, TOMS invoices must reference the special VAT regime in the FatturaPA XML. The document type code and VAT nature code must be set correctly for the Sistema di Interscambio (SDI) to accept the transmission. Progressive numbering must be maintained separately from standard invoices. The CRM handles all of this — the agent simply clicks "Generate Invoice" and the system produces a compliant FatturaPA XML ready for SDI transmission.

In France, the situation is evolving rapidly. From September 2026, all B2B invoices must be transmitted electronically via Chorus Pro or a certified platform. TOMS invoices use VAT category O (exempt with right of deduction) in the Factur-X format, with explicit reference to Article 266-1 of the Code General des Impots. The SIRET number is the mandatory legal identifier. French agencies must ensure their CRM generates Factur-X PDF/A-3 documents with correctly embedded CII XML.

Germany applies TOMS under Paragraph 25 of the Umsatzsteuergesetz (UStG), commonly referred to as Margenbesteuerung. The standard rate is 19%. ZUGFeRD invoices must reference this paragraph explicitly. The technical format is identical to Factur-X (both use CII XML embedded in PDF/A-3), but the legal references and identifier schemes differ.

Spain implements TOMS through Articles 141-147 of Ley 37/1992. The standard IVA rate is 21%. FacturaE 3.2.2 XML uses SpecialTaxableEvent code 02 to indicate the margin scheme. The NIF or CIF is the tax identifier, and country codes use ISO alpha-3 format (ESP, not ES). Spanish agencies must also consider the SII (Suministro Inmediato de Informacion) real-time reporting requirements.

A properly configured CRM detects the agency's country from the tenant profile and automatically applies the correct rate, legal references, and document format. The agent never needs to remember which paragraph of which law applies — the system handles it transparently.

Ready to modernise your agency?

itinovo CRM handles TOMS, quotes, invoicing, and supplier management — so you can focus on your clients.

Start free trial